Startups, I love you guys. You have so much passion and enthusiasm, and you’re hell-bent on changing the world, or at least the industry you’re in. I love you like nobody’s business, and if one of you would create a viable cloning machine so I could be in two places at once and crush my productivity goals I would probably empty my 401k, personal savings, and maybe even sell a kidney to fund the shit out of that.

As a startup, you’re (hopefully) experiencing massive growth but along with that growth comes a heaping mass of changes, and if there’s one universal truth about startups it’s that you’re all moving at lightning speed.

But the growth, changes, and speed don’t give you license to ignore key areas of your business.

As a marketing consultant I’ve worked with more than a handful of startups, been asked to invest in them, and before I started Hunt Interaction, I worked in the startup trenches for a time. I’ve seen startups rise and fall and I’m privy to many of their “inner workings.”

There are many factors that contribute to the life or death of a startup but focusing on the people, the inter-personal workings part of the startup equation is something that’s easy to overlook.

It’s easy to work IN your business - getting caught up in the small day-to-day stuff; it’s harder to work ON your business.

More...

successful startups tend to have these people-based philosophies in common.

1. Breathe, Calmly

Even though there’s crushing pressure to fund and ship the next greatest product you can’t move forward with a 100% “assholes and elbows” mentality. Yes, your burn rate is important, yes the competitive landscape is pressing, and yes, you need to secure your next round of funding. But you must stand up, look around and evaluate the current status and trajectory of your business.

Decisions rooted in panic or the heat of the moment are purely emotional and not logical and there’s probably enough emotion flying around your company to choke a team of therapists. Don't add to that mess.

2. Align Projects to Company Strategy

It’s tempting to pivot on projects or even the business when you don’t see instantaneous success or when a project isn’t moving fast enough.

Don’t.

You signed off on a path or a project because you believed in it and it aligned with your strategic goals (right? This is my semi-sarcastic way of telling you to align projects with your company goals and strategy). Killing a project before it has a chance to show you what it’s capable of is simply a waste of cash and time.

I could write a novel on when it's a good time to think about or actually pivot your business, that's not the point of this post, though.

There are always exceptions to killing off or pivoting on projects, but I’ve seen startups shift away from a key project, only to pick it up again 3 months later. *High five* for alienating and aggravating the people who were working on that project the first time around.

3. Trust Advisors

You vetted your advisors and trust they’re going to steer you in the right direction. Listen to them. If you don’t like the advice they’re dishing out, take a hard look at why you don’t like it.

If you don't like the advice because of a personal reason, get over yourself, suck it up, and get to work. If you legitimately believe they’re on the wrong path and giving you poor advice, fire them and get new advisors.

You don't have the luxury of wasting time when you're running a startup.

4. Invest in Real-World Market Validation

It’s not uncommon for the origin story of a startup to focus on a personal experience of one of the founders but this doesn’t mean that this experience is a universal one. It’s also not uncommon to see startups with market validations based on feedback from friends and family.

“Danger Will Robinson!” This is a dangerous road to hoe. Here’s why, your friends and family have an established relationship with you, they have skin in the relationship game. The odds are good that they value this relationship and won’t risk it by giving you an honest answer when you ask about your startup product.

Additionally, friends and family may not be your ideal target market (read also: willing to spend hard-earned cash) and basing your business foundation around half-correct and possibly misguided market information will lead you seriously astray and may even crush your company before it gets off the ground.

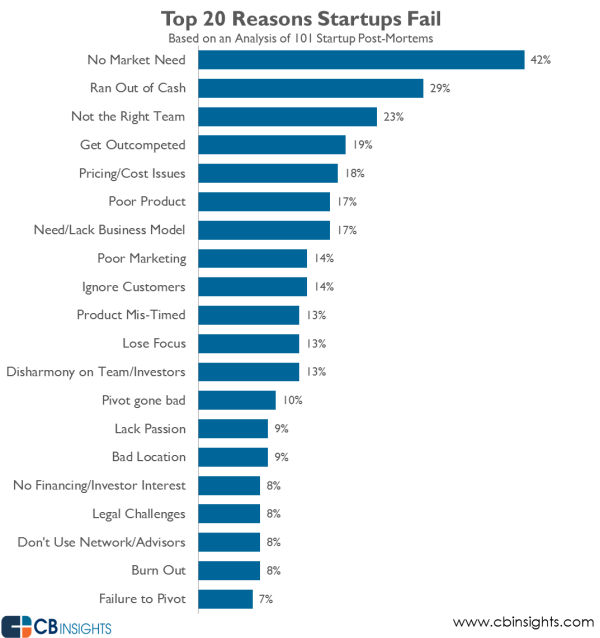

Don't believe me? A study of 101 startup post-mortems found that lack of market need is the #1 killer of startups. Wouldn't you rather know what the market really needs before you jump into the deep end?

4. Invest in Marketing Early

Startup marketing shouldn’t be an afterthought, though, in my experience, it usually is.

Your company can't afford to wait until the last critical moment before you need funding to invest in marketing. Marketing isn’t a “push button, get results” startup activity. Good marketing takes time and is an investment that can’t push to the back burner.

No, an intern who just graduated with an Art History degree doesn’t qualify as investing in marketing. Neither does hiring your sister-in-law who has an Instagram account with thousands of followers. This isn't to say they don't have great ideas, they just don't have the experience to create and execute on a company-wide strategy and you don't have time or the cash for them to learn on your startup dime.

(You could pick this cat or someone qualified to help with startup marketing, your choice)

Marketing is more than just branding, email newsletters, and social media posts. Good startup marketers have their finger on the pulse of your ideal target market and they can help you with projects like:

- market validation

- creating a value proposition and content that connects with customers

- competitive research

- crafting unique selling propositions

- user interface design feedback

- organizing and performing user testing of your product or service.

Good marketing can develop and execute on a user acquisition strategy that will knock your socks off and save you 3x what you’re currently paying. A Lower CAC always looks good to potential investors.

Startups who invest in marketing can continue the conversation with potential customers until they’re ready to buy (or you’re ready to launch). Keeping the lines of communication open and building your brand is critical for top-of-mind awareness and eventual conversion. The alternative is to fade into obscurity before you ever open your doors.

And a special note for technical founders - a good startup marketer can help you sell your idea to investors (translate tech-speak into English) and coach you on key selling points your target market will eat up once you launch. They can teach you how to speak non-technical English so you can communicate with business people and the regular “joe on the street” so they’ll understand what you’re saying without their brains melting.

Successful startups know that just because you built a company, doesn’t mean that people will be lined up, waiting to get in. You have to work for attention, attraction, and conversion.

5. "Check Yourself Before You Wreck Yourself"

When you have a company that’s your baby, and you’ve poured your heart, soul, and savings into making it work, it’s hard to check your ego at the door. But this is *exactly* what you must do to succeed.

90% of startup founders believe their product is going to “revolutionize” whatever market they’re in (yeah, I totally made that stat up). Only a small fraction of a percent of these founders get a chance to prove it.

As a founder, you focus on patents, groundbreaking technology, demand to put your personal welcome message on the homepage of your website, and when your customers don’t care, you’re bewildered. "Why don't they care about meeeee?"

Here’s the truth: Your customers don’t care about the same things you do. Your customers only care about how you solve a pain or a problem they’re having. Period. The end.

Co-founders will argue, they will disagree, but they must keep communicating with each other and finding points of collaboration and agreement. If co-founders aren’t getting along and creating friction, the company is headed for dark days. Founders have to check their egos and work together to move the company forward and divide their workload into important tasks and projects.

Your company exists for the sole purpose of solving a point of customer pain.

Swallow the humility pill whole, do not break, do not chew.

6. Keep Employees Happy

Employees make a sacrifice to work for you. Typically, they’ve accepted a reduced salary in exchange for equity, and they believe in the company and how it’s going to change the world. Don’t piss them off with off-strategy requests or yank projects from them before they’re done.

All the free soda in the world and the comfiest bean bag chairs won't overcome the risk your employees take to work in your startup. Treat their work with respect.

Talented people have other employment options, and the attrition will slow you down and cost you time and money.

Get the right people doing the right things. Startups need flexibility and cross-function cooperation, but if you’re dragging down your strategic advisors into tactical execution on a regular basis, you’re overpaying for their work product. Keep people doing what they do best. Don't ask your CTO to write blog posts and ask him/her to break down complex concepts into bite-sized chunks - the odds are good that taking this approach will produce a result that’s off target for your customers. Your CTO should be doing what they do best, anyway, not writing blog posts.

7. Offers Equity Selectively

You are not the Oprah of equity.

Be selective when you offer equity to people and vendors outside the immediate company. It’s understood that consultants and freelancers run their own businesses and businesses (much like yours) run on cash. They’re providing a valuable service to you doing what you can’t or don’t have time to do and bring a particular skill set that is valuable to you.

Smart consultants and freelancers understand the funding game and know that any shares they acquire in exchange for services will be diluted with the next round of funding. Respect their intelligence and honor this relationship with cash.

Keep the equity at home, where it belongs.

8. Organized Around the Revenue Model

Without revenue you don’t have a product, you have a funded and staffed hobby.

Successful startups have a fully-baked revenue plan, day 1 and work , every single day, towards implementing it.

Every goal, every objective in your company should lead back to revenue. If it doesn’t lead back to generating revenue, it shouldn't get done.

Answers such as “We don’t know how we’re going to make money yet” or “We're funded through ad/affiliate revenue” will get your butts thrown out of an investor pitch likety split, and rightly so.

There are a lot of numbers you need to know about your business, but at the very least you should know the following numbers:

- Revenue forecast (gross and net)

- Break-even point

- Revenue & Customer churn

- CAC (customer acquisition cost)

9. Focuses On a Specific Customer Segment

The smart startup knows everyone is not their customer.

Your company may have a product or service that everyone on the planet *could* find useful, but if you don’t start small, you’ll dilute your message and marketing budget and never reach the people who will buy, and love, your product.

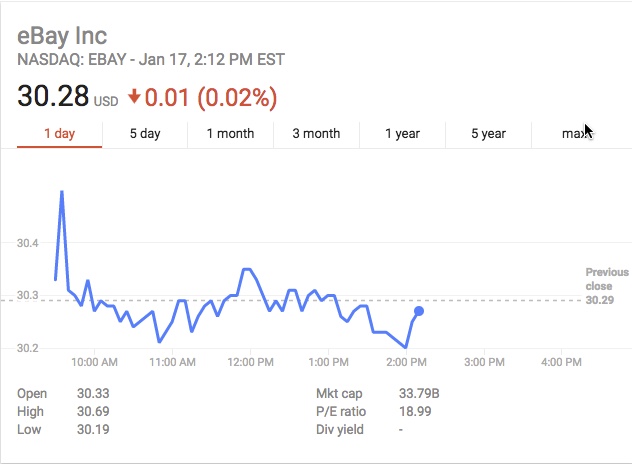

Even Ebay, a $27 billion dollar company has segmented their existing customers and potential customers and, even though they have a service everyone on the planet could use, they operate knowing that not everyone is going to use them.

10. Put Flexible Processes in Place

Startups who put light processes in place to ensure things don’t fall through the cracks help replicate successes and save time but allow enough flexibility to accommodate a rapidly changing business.

Screaming, “Startup!” is a poor excuse when you don’t have your shit together and a software release goes badly, or it’s not checked properly by your QA team.

It’s downright embarrassing to have your customers point out obvious bugs in your product or website; your embarrassment is compounded when 50 customers point it out on social media for the world to see.

Launching a startup and getting a it off the ground is no small feat, and I salute you and wish you much success. It’s painful to me to see a startup fold, and I'm never happy when that happens, because I know the level of effort it takes behind the scenes.

Startup success isn’t a fluke; it’s grounded in hard work and working smartly with the time and resources you have available to you.

There are many different aspects to launching and running a startup and this article only scratches the surface. Notice anything I missed? Shoot me an email and let's talk it out.